AI assistant

Invinity Energy Systems Plc Earnings Release 2025

6158_10-k_2026-06-01_c8a22cb3-7be2-4265-85dd-2515afac390b.html

Earnings Release

Open in viewerOpens in your device viewer

National Storage Mechanism | Additional information

RNS Number : 4055G

Invinity Energy Systems PLC

01 June 2026

1 June 2026

Invinity Energy Systems plc

("Invinity" or the "Company")

2025 Financial Results

Invinity Energy Systems plc (AIM: IES), a leading global manufacturer of utility-grade energy storage, announces its Full Year Results for the year ended 31 December 2025.

The Company will hold a virtual meeting for analysts at 9.30 a.m. today. Analysts wishing to attend are kindly requested to email [email protected] to receive dial-in details.

Invinity's management team will also host a results presentation and Q&A for all shareholders on Wednesday 3 June 2026 at 4.00 p.m. (UK). Those wishing to join the session can sign up to the Investor Meet Company platform for free via this link.

2025 Financial and Operational Highlights

· Revenue and Other Income of £8.7m and Project Grants* of £9.1m, totalling £17.8m (256% increase YoY - 2024: £5.0m).

· Sales of 31.4 MWh (504% increase YoY - 2024: 5.2 MWh).

· Product shipments totalling 24.9 MWh (241% increase YoY - 2024: 7.3 MWh).

· Gross Loss of £2.9m (17% reduction YoY - 2024: £3.5m).

· Total cash as at 31 December 2025: £28.8m (2024: £32.4m).

· The Group remains debt free.

*For all references to "Project Grants", please refer to Note 31 in the notes to the consolidated financial statements

Strategic Highlights

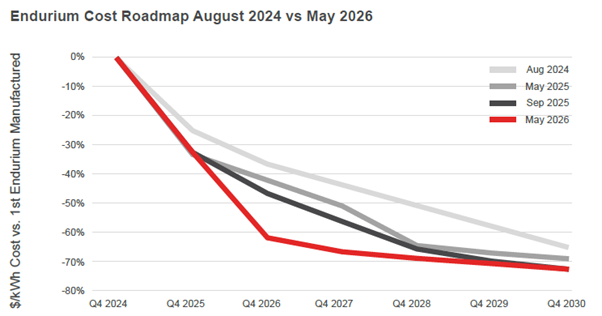

Cost - on target to achieve a forecast minimum 66% reduction in unit costs for Endurium versus our VS3 product within two years. Aggressive cost reduction achieved 18 months ahead of initial management expectations.

Customers - Tripled battery shipments from our factories against a backdrop of high-quality service delivered to our customers as evidenced by numerous public and private endorsements received.

Commercial - Six-fold increase in sales year-on-year, including the first sale of our new Endurium Enterprise product, and expanding our partnership network to gain access to some of the world's fastest growing markets (including India and China). Endurium has been included in 16.7 GWh of UK LDES Cap & Floor bids and our wider commercial opportunity pipeline also continues to grow, driven by improved product costs and performance and now contains a number of highly significant commercial, industrial and datacentre opportunities across Europe, North America and Asia.

Track Record - 9 GWh of energy has been dispatched by our products globally to date. Projects using our batteries are now increasingly backed by third party lending and we have continued to improve our bankability credentials through third-party technical studies and validation.

Scale - Manufacturing capabilities were expanded during the year as well as enhancing our quality control and supply chain functions.

Post Period:

· Invinity selected to design a 1.5 GWh VFB system for FlexBase Group project in Switzerland. Engineering design phase of the project now underway.

· Delivery of all VFBs to Copwood VFB Energy Hub completed in May 2026 ahead of anticipated grid-connection and the commencement of operations later in 2026.

· 2 MWh sale to a C&I project in Wisconsin, USA as part of a U.S. Department of Energy-funded project.

The Company's 2025 Annual Report will soon be available to be downloaded from the Investor section of the website.

Jonathan Marren, Chief Executive Officer at Invinity said:

"I am immensely proud of the progress delivered across Invinity during 2025 and into the current year. The results reflect a business that has deliberately invested in its foundations and is now clearly entering a new phase of accelerating growth.

"Over the past year, we have taken meaningful steps to remove the barriers to scale - significantly reducing product costs, increasing unit shipments and growing sales while expanding our reach through strategic partnerships into some of the world's fastest growing energy storage markets. These efforts are now translating into tangible commercial momentum, with a growing pipeline of opportunities across multiple geographies and customer segments.

"At the same time, confidence in our technology continues to build, with a growing base of satisfied customers and flagship projects such as the Copwood VFB Energy Hub and FlexBase's Technology Centre Laufenburg increasingly demonstrating Invinity's credentials as a trusted partner capable of delivering at scale.

As the world demands cheaper, more secure energy, the opportunity ahead is clear. With momentum building and strong foundations in place, I am incredibly excited for what comes next."

Stay up to date with news from Invinity. Join the distribution list for the Company's monthly investor newsletter here.

Enquiries:

| Invinity Energy Systems plc | +44 (0)20 4551 0361 |

| Jonathan Marren, Chief Executive Officer Joe Worthington, Senior Director, Corporate Affairs |

|

| Canaccord Genuity (Nominated Adviser and Joint Broker) | +44 (0)20 7523 8000 |

| Henry Fitzgerald-O'Connor / Harry Pardoe / Charlie Hammond | |

| VSA Capital (Joint Broker) | +44 (0)20 3005 5000 |

| Andrew Monk / Andrew Raca |

Notes to Editors

Invinity Energy Systems plc (AIM: IES) is a world-leading manufacturer of vanadium flow batteries for energy storage. Built in our factories in the UK and Canada, the Company's proven, commercialised, longer duration energy storage technology has been deployed at scale and dispatched gigawatt-hours of electricity for customers across the world.

Invinity's safe, scalable and durable battery technology is a trusted and safer alternative to lithium-ion batteries. Endurium VFBs are engineered for heavy-duty, high throughput applications, they don't wear out, cannot catch fire and are designed to be operated for 30 years or more. Our products address the challenges of our global energy system, unlocking the power of renewable generation by delivering energy storage without limits.

To find out more, visit invinity.com, sign up to our monthly Investor Newsletter here or contact Investor Relations on via +44 (0)20 4551 0361 or [email protected].

Audited Financial Results for the Year Ended 31 December 2025

Chair's Report

Powering the Future: Meeting the Needs of a Modern Network

The abundance of cheap, clean power in electric grids is breaking records everywhere. 2025 saw renewables provide more than 50% of UK power generation for the second year running and growth forecasts outline that the world will get 50% of its power from renewables by 2030. This is undeniable proof that the world wants clean, low-cost renewable power and the Invinity team remains focused on providing an economic energy storage solution which will be a critical part of our energy future.

I'm pleased to note that Invinity's core technology, capable of providing both high-throughput and longer duration energy storage, is now increasingly a part of modern power system infrastructure. The requirement for flexible, dispatchable, low-carbon energy storage capacity in our electric grids has shifted from aspiration to necessity.

Numerous policies across the UK, North America and Europe are actively accelerating the deployment of long duration energy storage (LDES) batteries. Securing energy sovereignty is a key foreign and domestic policy objective for governments across the world, as is generating the electricity needed to power the increasing electrification of industry and transport. It's beyond doubt that both the deployment and use of low-cost, low-carbon, 24/7 renewable energy powers growth in economies today and to this end, our team continues to participate in strategic dialogues with governments in our key markets.

Importantly, there has been much commercial progress during the period. Jonathan Marren's Chief Executive report gives greater detail but I would wish to highlight the expansion of our existing Endurium product range, with the launch of our Enterprise product in September, and the team's notable achievements in product cost reductions. I am pleased to report that Jonathan, the broader senior leadership group, and the entire Invinity team continue to make important progress in achieving our long-term strategy.

Partnerships were a key feature of 2025 and the relationships Invinity has developed over recent years have provided numerous benefits to the Company. They have not only enhanced our reputation in the industry but augmented our offering to customers. Our relationship with Gamesa Electric, now part of ABB Renewable Energy, enabled the first deployment of our Endurium product at a site where the product has met or exceeded our expectations in operation. The backing of National Wealth Fund (NWF), alongside funding from the Department of Energy Security and Net Zero (DESNZ), has enabled us to deploy the Copwood VFB Energy Hub (formerly the LoDES project) - the UK's largest LDES battery and an important strategic asset for the Company. Furthermore, the development of our relationship with Atri Energy Transition (Atri Energy) has opened up numerous opportunities in the Indian market and our growing partnerships in China and Hong Kong with UESNT, C&D Inc. and International Resources Limited (IRL) are supportive to key corporate objectives such as our product cost reduction programme.

These local partners are key to our ability to scale to meet growing demand for our product. Energy storage markets are inherently regional: regulatory frameworks, grid requirements and customer expectations differ significantly by country. To succeed at scale requires strong local presence and Invinity's approach prioritises in-country partnerships to deliver competitive pricing, secure supply chains and ensure best-in-class customer support. Local production also reduces logistical risk, enhances eligibility for domestic content incentives and demonstrates long-term commitment to host markets, all of which is highly valued by governments, policymakers and above all else, our customers.

Product leadership is core to our success. Our products are designed to address the full spectrum of our customers' needs, from large-scale renewable generators to energy intensive Commercial & Industrial (C&I) applications and datacentres. I'm delighted that we recently reached 9 GWh of electricity dispatched by our batteries in service for our customers. The launch of our Endurium product has enabled us to sell into significantly larger projects, including the recently announced GWh-scale VFB for our new partner FlexBase Group in Switzerland, and at the same time open up major opportunities in large-scale procurement schemes such as those we have been selected for through the UK's LDES Cap & Floor Scheme. Furthermore, our Enterprise product continues to gain traction in the C&I space, with our first sale announced in late 2025 to a French aquaculture business.

These important steps were supported by the appointment of Dr. Margaret Amos to Invinity's Board in June, who brings valuable financial and business expertise. Additionally, the completion of the redomiciliation earlier in the year has opened up a number of opportunities to streamline our corporate structure and simplify our operations to better manage our long-term growth. This move also enabled our long-standing Board member, Michael Farrow, to retire in 2025. My sincere thanks go to him, on behalf of the Board and all Invinity, for his guidance over his many years of service and we wish him the very best in his retirement.

I firmly believe that Invinity remains on the right course towards success. We are now better structured for long-term growth, have the support of strong global and regional partners and have commercialised a technology which offers a solution to one of the most pressing issues the global energy market is facing. Our leadership in this industry has positioned us strongly for the future. To succeed, we must continue to execute on the opportunity we have created and I remain confident that under the leadership of Jonathan, Adam and Matt, Invinity is ready not only to participate in the next phase of the energy transition, but to help lead it.

Neil O'Brien

Non-Executive Chair

29 May 2026

CEO Report:

Charging Ahead: A Year of Progress Across Our Five Strategic Pillars

I am immensely proud of the progress made across the business throughout 2025 and into the current year. More important than any single metric or achievement, however, is what that progress represents: a business that has deliberately invested in its foundations and is now positioned for its next phase of accelerated, sustainable growth.

Over the period and in the year to date, we have made significant reductions to the cost of our flagship Endurium product, increased battery sales sixfold year‑on‑year, more than tripled product shipments from our factories and expanded our network of strategic partnerships to access some of the world's fastest‑growing energy storage markets. These achievements reflect not just operational progress, but evidence the focus we have placed on removing constraints that limit our ability to scale.

At the same time, we continued to build an increasingly compelling commercial pipeline, including opportunities across multiple geographies and customer segments. Encouragingly, we are also seeing increased demand from existing customers who return to Invinity because they trust us to deliver reliably, competitively and at scale. For me, this trust, earned through performance, is the strongest validation of both our technology and our people.

By combining world‑class flow battery technology, the highest standards of customer service and aggressive cost reduction, we are positioning Invinity to compete effectively, win more business and deliver long‑term value for all stakeholders as the business grows and matures.

Our progress has been defined by relentless, disciplined focus across five core strategic pillars. Our achievements in these areas, delivered across 2025 and during the current year to date, are driving Invinity's journey from a niche market challenger that was constrained by product costs and capacity towards a global leader within a fast growing and extremely exciting market segment. There is still a long way to go, with significant challenges to overcome, but I'm delighted to report on material steps forward achieved during the year.

Our Strategic Pillars

Revenue and Project Grants*

Achieving consistent revenue growth remains critical at this stage of our journey. I am therefore pleased that the team delivered a 256% year‑on‑year increase in total revenue and Project Grants* to £17.8 million in 2025.

This performance reflects deliveries to customers across Europe and the USA, in addition to continued progress on the Invinity Copwood VFB Energy Hub ("Copwood") project in the UK, our largest delivered to date. Supported by the Department for Energy Security and Net Zero and the National Wealth Fund, we began construction of Copwood during 2025 and with all batteries now on site, we are incredibly excited to bring Europe's largest collocated vanadium flow battery online later this year.

Beyond its financial contribution (both in terms of grant income for the year in review and in terms of future cashflow for the business), Copwood is strategically important: it strengthens our delivery credentials, enhances bankability and provides a powerful reference asset. It will be a critical source of real‑world operating data, enabling customers, investors and policymakers to see Invinity's technology delivering value at scale.

Product

2025 marked an important year of external validation for our products. ABB Renewable Energy's successful testing of our first Endurium VFB at La Plana provided critical field‑level confirmation of Endurium's performance at a time when long‑duration energy storage (LDES) is moving rapidly from concept to deployment.

Our disciplined focus on operational and technical excellence is an important strength of Invinity, the results of which include highly positive feedback from customers and the consistent achievement of high technical scores in competitive tendering processes. Further confidence was reinforced during the year in review in the form of product validation reports from DNV, helping to further underpin discussions with prospective partners and financiers as we continue to grow and develop as a business.

The year also saw the launch of Endurium Enterprise, expanding our value proposition for Commercial & Industrial (C&I) customers. Our first Enterprise sale, to a French business in December 2025, was an important milestone, validating our strategy and opening a meaningful new market segment for future growth.

Commercial

Commercial momentum accelerated significantly during the year, with 31.4 MWh of sales announced - a sixfold increase in booked orders year‑on‑year. This significant improvement was achieved as a result of a number of factors including improvements in cost and technical performance flowing through to our commercial proposals, as well the investment we have made in our global commercial team who are deepening our customer relationships and building a significant commercial pipeline that includes a number of highly significant commercial, industrial and datacentre opportunities in Europe, North America and Asia. To this end, we were delighted to recently announce that Invinity has been selected by FlexBase Group to design and deliver an up to 1.5 GWh flow battery - the world's largest to date - for use at their Technology Centre Laufenburg project in Switzerland, supporting an AI datacentre and technology campus as well as providing stabilisation services for the local grid. This project represents a significant step-change in the scale of commercial opportunities for Invinity and is an important indicator for growing demand in our sector.

This growing demand, combined with the launch of a number of large-scale procurement schemes in the LDES space during the year, contributed to a 73% year‑on‑year increase in average commercial deal size. The most notable scheme that was launched was the UK's LDES Cap and Floor Scheme, through which 16.7 GWh of Invinity batteries across 21 bids secured eligibility status through collaborations with partners including Frontier Power. This outcome strongly reinforces our technology's suitability for large‑scale, government‑backed projects - another key target market.

Cost

As prices continue to fall across the energy storage sector, cost competitiveness remains fundamental to success. Under the leadership of our President, Matt Harper, the team is on target to achieve a forecast minimum 66% reduction in unit costs for Endurium versus our VS3 product within two years. Removing two-thirds of the cost from our product in less than two years is an incredible achievement and is the product of a multi‑faceted strategy encompassing value engineering, higher‑volume manufacturing processes and a significantly strengthened supply chain.

The majority of the programme is now close to completion, roughly 18 months ahead of our initial expectations, and has already materially reduced the sale price of our products, helping to improve our commercial prospects by opening up new markets.

Our strategic partnerships, including with UESNT, Atri and C&D Inc, which continued to develop strongly throughout the year in review, will also support our cost down efforts through the implementation of our relatively low‑capex, partnership‑led manufacturing model. This approach allows Invinity to access best‑cost regions, supports local content requirements and enables us to scale efficiently as demand grows.

Capital

Maintaining financial discipline has been a consistent priority. Under CFO Adam Howard's leadership, we continued to streamline our corporate structure following the redomiciliation, reducing overheads and improving transparency.

The implementation of a new Enterprise Resource Planning ("ERP") system is simplifying processes across supply chain, finance and customer‑facing functions, while helping to identify further efficiencies as we scale.

In September, the £25 million Subscription from Atri Energy and Next Gen Mobility strengthened our working capital position and opened significant commercial and operational opportunities in India, a relationship we expect to deepen over time.

Navigating the Age of Electricity

The world is entering what many describe as the "Age of Electricity". Electrification across AI, air conditioning and electric vehicles is driving unprecedented demand growth, while ongoing geopolitical events ensure that energy security and sovereignty remain high on national agendas across the world.

The defining challenge is no longer simply generation. It is aligning abundant, variable renewable energy with increasingly complex demand profiles. Invinity's technology sits at the centre of this challenge, enabling greater energy security, unlocking renewable potential and helping to lower long‑term system costs, which ultimately means lower energy bills for households and businesses.

A Leading Voice in the LDES Industry

Invinity continues to play an active role in shaping the global LDES conversation. Throughout the year, we engaged extensively with governments and policymakers across the UK, Canada, China, India and the USA, reinforcing our position as both a technology leader and a trusted delivery partner.

These engagements, from ministerial visits to our UK facilities to collaborations with U.S. national laboratories, enhance our credibility and influence, while supporting the broader development of the LDES market globally.

Summary and Outlook

As outlined in the Strategy section of our Annual Report, we have a clear path toward establishing Endurium as the de facto technology choice for stationary energy storage globally.

The progress delivered during 2025 and into this year represents a step change in Invinity's ability to deliver at scale. Cost barriers have come down, delivery credibility has risen, technical bankability has been strengthened and, critically, a substantial pipeline and value proposition have been built behind the scenes.

Our primary challenge now is delivery at scale: converting preparation into momentum, pipeline into revenue and capability into self-sustaining growth. While there remains work ahead, particularly in driving manufacturing volumes, further reducing costs and reaching cashflow break‑even, the foundations are firmly in place.

My thanks go to Matt, Adam, the Board and the entire Invinity team for their dedication, as well as to our partners and customers for their trust.

As the world demands cheaper, more secure energy, the opportunity ahead of us is immense and we are moving faster than ever to stay at the forefront of this transition and capture maximum value for our stakeholders. We have the momentum, we have the foundation, and I am incredibly excited for what comes next.

Jonathan Marren

Chief Executive Officer

29 May 2026

CFO Report:

Cost Down Supporting Margin Growth

The financial performance of the Group during 2025 reflected a period of continued operational progress and financial transition as the Company advanced the commercialisation of its Endurium product platform while continuing to deliver against its project pipeline.

| 2025 | 2024 | 2023 | |

| Year to 31 December | £m | £m | £m |

| Revenue | 8.2 | 5.0 | 22.0 |

| Other Items of Income | 0.5 | 0.2 | - |

| Project Grants* | 9.1 | 0.3 | |

| Total Revenue & Project Grants* | 17.8 | 5.2 | 22.3 |

| Gross (Loss)/Profit | (2.9) | (3.5) | (3.3) |

| Adjusted EBITDA | (20.6) | (19.3) | (22.3) |

| Pre-tax Loss | (24.1) | (22.8) | (23.2) |

| Property, Plant and Equipment | 10.4 | 2.3 | 1.7 |

| Total Inventory and Pre-paid Inventory | 4.0 | 8.3 | 4.4 |

| Net Cash | 28.8 | 32.4 | 5.0 |

| Year to 31 December | 2025 £m |

2024 £m |

2023 £m |

| Loss from operations | (24.6) | (24.1) | (22.8) |

| Add back (deduct): | |||

| Depreciation and amortisation | 1.2 | 1.3 | 1.1 |

| Impairment of inventory and supplier deposits | 0.5 | 0.4 | 0.3 |

| Share based payment charges | 0.8 | 0.6 | 0.7 |

| Warranty and onerous contract provisions | 1.5 | 2.1 | (1.7) |

| Other Adjusting Items, net 1 | - | 0.4 | 0.2 |

| Adjusted EBITDA | (20.6) | (19.3) | (22.3) |

1. Other Adjusting Items, net, includes gain and loss on disposal of non-current assets and legal settlements, and redomiciliation costs.

Total Revenue and Project Grants* increased to £17.8 million in 2025 from £5.2 million in 2024. This movement reflected increased activity across customer projects, the contribution of royalty income recognised during the year, and £9.1 million of Project Grants* from the Copwood VFB Energy Hub project ("Copwood"). Gross profit margin improved from -70% to -35% and as a result, the Group recorded an improvement in gross loss of £2.9 million, from £3.5 million in 2024. The improvement in gross margin reflects early evidence of improving product economics through cost down initiatives.

Administrative expenses increased to £21.9 million in 2025 from £20.3 million in 2024. The increase reflected continued investment in commercialisation, product certification, supplier development and organisational capability to support the Endurium product platform, together with share-based payment charges reflecting equity incentives. Operating costs remained an area of active management focus throughout the year.

Loss from operations of £24.6 million is a 2% increase over the prior year loss of £24.1 million, and the bottom line loss for the year increased to £24.1 million from £22.8 million largely reflecting the decrease in net finance income of £0.5 million compared to £1.3 million in 2024.

The Group's key focus remains on further reducing the cost of its Endurium product in order to expand its addressable commercial market. During 2025, Endurium units shipped at a materially lower product cost than the previous generation VS3 product.

2025 Cash Performance

Net Cash Outflow from Operating Activities improved from £24.9 million to £17.2 million largely reflecting changes in working capital and the release of inventory for the Copwood project.

Investing cash outflows increased to £9.5 million compared with £1.3 million in 2024, primarily reflecting investment into Copwood and Invinity's manufacturing capacity, including the purchase and commissioning of a semi-automated stack production line. Capital and related prepaid expenditure of £17.0 million was partly offset by the £7.5 million of grant income received for Copwood in 2025.

During the year, the Group recorded £9.1 million of DESNZ Project Grants relating to Copwood in addition to the £0.3m in 2023. Of this, £7.7 million cash was received during the year and the remaining £2 million of the full £10 million award was received in 2026. In accordance with the Group's accounting policies, grant support has been recognised through a combination of offsets against qualifying capital expenditure and deferred income reflecting the timing and nature of the related project costs.

Financing cash inflows were £23.4 million in 2025 compared with £53.6 million in 2024, reflecting proceeds from the £25.0 million subscription offset by transaction costs and lease payments.

| Project Grants* | £m |

| Grant income recognised against capital assets | 6.7 |

| Grant income recognised against other items of operating income | 0.6 |

| Grant income deferred | 1.8 |

| Total Project Grants* | 9.1 |

* Project Grants means project grant funding received and claimed from DESNZ. This includes a deferred liability of £1.8 million, because at the year-end Invinity was still manufacturing the batteries and subsequent to the year end the batteries were delivered. Refer to note 31 for details

Liquidity, Funding and Net Working Capital

The Group ended the year with cash and cash equivalents of £28.8 million at 31 December 2025 compared with £32.4 million at 31 December 2024. Management continues to monitor downside risks closely and retains flexibility to reduce discretionary capital expenditure and tightly manage operating costs should project timing or revenue conversion be delayed.

| 2025 £m |

2024 £m |

2023 £m |

|

| Total inventory | 2.6 | 5.8 | 3.3 |

| Total pre-paid inventory | 1.4 | 2.5 | 1.1 |

| Total Inventory and Pre-paid Inventory | 4.0 | 8.3 | 4.4 |

| Amounts due from customer contracts | 3.3 | 0.8 | 2.5 |

| Receivable from supplier arrangement | 1.9 | - | - |

| Government grant receivable (Copwood) | 1.4 | - | - |

| Contract assets3 | 1.2 | 1.1 | 1.2 |

| Contract liabilities4 | (0.6) | (1.4) | (1.3) |

| Trade payables | (5.6) | (3.0) | (2.2) |

| Provision for contract losses | (2.2) | (1.9) | (0.3) |

| Warranty provision | (0.2) | (0.1) | (0.6) |

| Net Operating Position5 | 3.2 | 3.8 | 3.6 |

3 Contract assets includes accrued income for work done not yet received

4 Contract liabilities includes deferred revenue related to advances on customer contracts

5 Net Operating Position considers wider balance sheet items directly relating to product sales including the Copwood project delivery.

Net Operating Position decreased from £3.8 million in 2024 to £3.2 million in 2025 because of reduced inventory levels primarily reflecting Copwood and increased trade payables of £2.6 million which reflected the timing of supplier invoices received in the final weeks of the year. The decrease in net position was offset largely by a £5.8 million increase in trade, supplier and grant receivables.

Total provisions increased to £2.4 million in 2025 from £2.0 million in 2024 These warranty costs relate to provisions required to service legacy systems and elevated logistics and shipping costs associated with specific project delivery to two remote sites.

Going Concern

The Directors have made an assessment of going concern covering the period from the date of approval of the financial statements to June 2027 and in making this statement, have prepared a cash flow forecast covering this period. The Directors have also considered whether there are any significant events expected to arise beyond the going concern period.

The forecast indicates that the Group expects to remain cash positive during the going concern period, without the requirement for further fundraising. This forecast includes judgements and estimates regarding income from pipeline projects, expected costs of delivering the contracts, and cost mitigation measures including the deferral of discretionary expenditure.

In order to fund expansion of the business, the Directors anticipate that additional funding would be required. The Directors have considered the availability of potential funding sources and the Group's track record in accessing capital markets in forming this assessment.

Invinity has prepared a downside cash forecast for the purposes of the going concern evaluation, which excludes all pipeline contracts that are not yet signed. In this scenario, the forecast assumes a reduction or deferral of costs in order to preserve cash without additional funding. If required, the Directors consider that the Group has the ability to reduce or defer costs without adversely affecting the short-term delivery of contracted income in downside forecast. The outcome of this scenario is that the Company has sufficient cash through the going concern period.

On the basis of this assessment, the Directors are satisfied that the Group has sufficient resources to continue in operation for the going concern period. Accordingly, the financial statements have been prepared on a going concern basis.

Adam Howard

Chief Financial Officer

29 May 2026

President's Report:

Solving Our Customers' Energy Needs

It wasn't long ago that few of us questioned the reliable, low-cost supply of electricity to our homes and businesses. Demand was flat, transmission and distribution grids were reliable, and low-cost power from fuel-based generating assets backed by robust supply chains were the cornerstone of our generating fleet.

Contrast that with today, where energy costs are a major concern in everything from family budgets to corporate strategies. In Great Britain, typical household electricity bills remain on average 42% higher than the winter of 2022. Commercial electricity prices have similarly risen, and by late 2025 were current sitting around 75% above early-2021 averages, reinforcing the need for solutions that improve security of supply and cost predictability.

This dramatic shift has its origins on both the supply and demand sides of our electricity system. Input prices, particularly those tied to natural gas, are increasing supply costs, while electricity demand is increasing even in mature economies for the first time in a generation. But it isn't just average prices, or average demand: Volatility is also on the rise. Geopolitical tensions are triggering whipsaws within global fuels supply chains. The lowest-cost source of new generation is fundamentally intermittent renewable power. And the largest new loads of our modern economy, datacentres, are exhibiting load profiles that are far more stochastic than the dark satanic mills of old.

These trends seem unlikely to end soon. Electricity demand will continue to rise as transport, heating, industry and digital infrastructure electrify. The International Energy Agency expects global electricity demand to grow at least ~4% per year on average through 2030, with emerging markets driving the majority of growth and advanced economies returning to expansion after decades of stagnation.

Supply is an equal challenge. While low-cost solar and wind are scaling quickly, their intermittent nature is stressing the grid as never before, with flexibility and capacity now as critical as bulk electricity supply. Moreover, these assets are often located away from major demand centres, and installing new transmission and distribution build-out is costly and slow.

Together, these forces are leading participants both on the supply and demand side of the industry to look to new solutions to ensure they continue to enjoy reliable, safe, low-cost electricity. Increasingly, energy storage is viewed as one of the most deployable, flexible and low-cost of those solutions.

On the front lines: Generators, Industry and Datacentres

Generators

The falling costs of renewable generation means it is increasingly the dominant power source being built today. Whether projects are the result of utility procurements targeted at specific generation types, or of developers seeking to deliver electrons to wholesale markets at the lowest possible cost, solar and wind power are leading an unprecedented shift. In the UK, sustained wind and solar build-out means renewables now supply more than half of annual electricity generation. As penetration rises, the need to firm variable generation becomes a larger and more investable part of the value chain.

But limits are beginning to emerge; and at Invinity, we get to see first-hand globally how regulators, utilities and generators are adapting. Renewable generation now outstrips consumption in South Australia on a regular basis; for example, the fourth quarter of 2025 saw negative electricity prices in that state a staggering 47.4% of the time. This has significantly enhanced revenues for our customer Yadlamalka Energy from their Spencer Energy solar-plus-storage project.

In California, regulators have taken a different approach by requiring a certain amount of storage to be installed by regulated utilities, with the goal of absorbing excess solar generation then dispatching that energy into evening peaks and so reducing dependence on expensive gas-fired peaking generation. This requirement has led to a massive expansion of California's battery fleet, from 1.3 GW in 2021 to over 17 GW at present. The results speak for themselves: Peak electricity rates in 2022 exceeded $70/kWh over 14% of the time, but by 2025 almost never reached that level. This served not only to help cap electricity users' costs but put a floor under the price at which solar generation was valued in wholesale markets.

Commercial & Industrial Customers

Increasing energy prices affects commercial and industrial users significantly. With no real way to control grid electricity prices and having the continued profitable operation of their businesses as by far their primary focus, they've long been seen as important but passive players in the electricity system.

The shift from a centralised to a more distributed paradigm within the electricity system has changed that. Recent years have seen individual companies participate either by engaging in demand reduction programmes, or by building their own on-site generation capacity, often using solar PV generation.

From Scottish Water's site at Perth, to the recently commissioned Viejas Resort and Casino in Southern California, Invinity has long helped businesses reduce their electricity costs. Many of our early deployments were intended to enhance decarbonisation efforts; more recently, ever-cheaper solar panels have enhanced how our batteries and PV together can significantly lower energy costs and reduce exposure to volatile power markets. In parallel, resilience has become a more prominent driver as many sites seek greater control over critical power supply.

What we hear from all site operators is that no matter the economic impact, safety is paramount. No amount of electricity savings will compensate for the impact of a fire at site, or injury to personnel. Such concerns are leading many of the facility operators we speak with to reconsider deploying lithium-ion systems close to critical facilities or large workforces. These concerns are further enhancing their interest in our storage solutions because they enjoy significantly a lower operational risk profile.

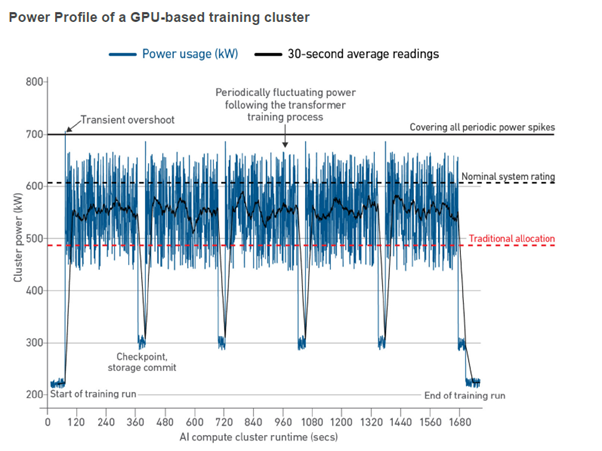

Datacentres

Growth in AI, cloud computing and digital services is driving a step-change in electricity demand from datacentres. AI learning workloads are already creating larger and faster load swings than more traditional cloud computing applications, since the tasks are synchronized to achieve maximum effect. This means whole datacentre loads can fluctuate from zero to 100% of rated power draw on a second-by-second basis. Batteries can help with this, but the duty cycle is punishing. Frequent full charge-to-discharge swings will dramatically accelerate degradation of conventional lithium batteries.

Source: https://journal.uptimeinstitute.com/electrical-considerations-with-large-ai-compute/

Datacentre operators have consistently viewed securing reliable access to low-cost power as a main driver for where these facilities can be located, and how much computing power they can include. Connection queues and lead times frequently shape deployment plans, with some projects unable to secure grid capacity to match intended commissioning dates. As a result, many datacentre developers and operators are evaluating on-site generation paired with storage to improve certainty of supply, maintain resilience and reduce exposure to peak pricing.

Different purposes, but common needs

There are common themes that emerge when talking with our existing and potential customers about how they are, or expect to, make ever more valuable use of our batteries. Broadly, those include the ability to cycle frequently, dispatch flexibly, be easy to permit and install, and to reliably deliver their intended use for years or even decades.

Cycling regularly enables energy storage assets to supply electricity when generation is unavailable or insufficient and absorbs excess generation when it is abundant. In many operating regimes, that means cycling more than once per day to firm renewables and support grid and site-level flexibility. AI datacentres are pushing this to the extreme, with cycle times in minutes and ramp rates consistently measured in milliseconds.

Flexibility is equally important, as simply being able to charge and discharge doesn't meet the needs of many users. From solar power generators looking to absorb swings in PV output, to datacentre operators looking to manage shifting loads, maximising operational flexibility without limiting performance or durability irrespective of a battery's state of charge is key to maximising the jobs a battery can do for its owners.

Permitting can be a gating factor for storage projects, influencing timelines, cost and the ability to install in certain regions. Some technologies require extensive safety mitigations to address fire risk and environmental concerns, adding time, cost and complexity. Noise considerations can also influence approvals, particularly near urban centres. And in some regions, local or regional governments have adopted statues banning certain batteries outright, citing fire safety concerns.

Longevity is critical as our electric grid depends on equipment designed to operate for decades. As demand rises and systems rely more heavily on storage, customers and investors place increasing value on solutions that can sustain performance over long operating lives. Moreover, durable assets mean predictable operating costs and avoided refurbishment or augmentation costs, improving return-on-investment while minimising lifecycle environmental impacts.

Storage capacity is the fundamental measure of any battery's performance, but many grid-connected storage technologies capacity degrades significantly over time. This can mean additional augmentation or replacement, especially when customers need their batteries to cycle frequently. For multi-decade assets, retaining usable capacity is a material decision factor. Technologies that sustain capacity and performance can reduce lifetime cost and operational uncertainty. Consistency supports underwriting and planning confidence for operators and investors across long operating horizons.

Invinity's VFBs - The tie that binds

Invinity's VFBs are already serving customers all over the world. Our Endurium and Endurium Enterprise products have proven their ability to cycle better with fewer operating restrictions, be easier to permit and last longer than the lithium-ion batteries being deployed into similar applications.

As long-duration storage moves from pilot activity to scaled procurement, we know that our products combine durability, a strong safety profile and predictable lifetime performance and can deliver a meaningful advantage to our customers. Why?

· Because they're built for durability and flexibility, performing in the most demanding applications while delivering limitless cycles over decades of service;

· because they have materially better environmental credentials and high recyclability while facilitating easier permitting;

· because they are scalable across a wide variety of project sizes, sites and climatic conditions; and

· because over and over again, our customers tell us how our vanadium flow batteries have outperformed expectations, delivering capabilities above and beyond what they were originally intended to do.

Manufactured in Britain and Canada, Invinity's Endurium VFBs are ideally positioned to support the grid by enhancing reliability, reduce reliance on expensive fossil generation and unlock higher renewable penetration. Behind the meter, they offer a uniquely capable solution for controlling loads from factories and datacentres, without the unknowns around fire safety, permitting and operating life that are lithium's hallmarks. As energy storage continues to prove its place as the cornerstone of the future of electricity supply and demand, Invinity's batteries are increasingly obvious as the right choice.

Matt Harper

President

29 May 2026

Financial Statements

Consolidated Statement of Profit and Loss

For the year ended 31 December 2025

| 2025 | 2024 (Unaudited)1 | ||

| Note | £000 | £000 | |

| Revenue | 4 | 8,182 | 5,015 |

| Cost of Sales | 5 | (11,047) | (8,528) |

| Gross Loss | (2,865) | (3,513) | |

| Operating Costs | |||

| Administrative expenses | 6 | (21,895) | (20,334) |

| Other items of operating income | 10 | 1,092 | 236 |

| Other items of operating expense | 10 | (950) | (446) |

| Loss from Operations | (24,618) | (24,057) | |

| Finance income | 11 | 843 | 1,358 |

| Finance costs | 11 | (147) | (106) |

| (Loss)/Gain on foreign currency transactions | 11 | (172) | 8 |

| Net Finance Income | 524 | 1,260 | |

| Loss Before Income Tax | (24,094) | (22,797) | |

| Income tax expense | 12 | - | - |

| Loss for the Year | (24,094) | (22,797) | |

| Loss per Ordinary Share in Pence | |||

| Basic | 13 | (5.1) | (6.7) |

| Diluted | 13 | (5.1) | (6.7) |

1Refer to note 1

The above consolidated statement of profit and loss should be read in conjunction with the accompanying notes.

Consolidated Statement of Comprehensive Income

For the year ended 31 December 2025

| 2025 | 2024 (Unaudited)1 | ||

| £000 | £000 | ||

| Loss for the Year Other Comprehensive Expense Items that may be Reclassified Subsequently to Profit or Loss: |

(24,094) | (22,797) | |

| Exchange differences on the translation of foreign operations | (96) | (355) | |

| Total Comprehensive Loss for the Year | (24,190) | (23,152) |

1Refer to note 1

The above consolidated statement of comprehensive income should be read in conjunction with the accompanying notes.

Consolidated Statement of Financial Position

As at 31 December 2025

| 2025 | 2024 (Unaudited)1 | ||

| Note | £000 | £000 | |

| Non-Current Assets | |||

| Goodwill and other intangible assets | 15 | 23,948 | 23,959 |

| Property, plant and equipment | 16 | 10,360 | 2,346 |

| Right-of-use assets | 17 | 1,640 | 1,526 |

| Contract assets | 21 | 225 | - |

| Other non-current assets | 19 | 191 | - |

| Total Non-Current Assets | 36,364 | 27,831 | |

| Current Assets | |||

| Inventory | 20 | 2,636 | 5,753 |

| Contract assets | 21 | 978 | 1,149 |

| Trade receivables | 22 | 3,260 | 827 |

| Other current assets | 23 | 9,019 | 7,648 |

| Cash and cash equivalents | 24 | 28,789 | 32,352 |

| Total Current Assets | 44,682 | 47,729 | |

| Total Assets | 81,046 | 75,560 | |

| Current Liabilities | |||

| Trade and other payables | 25 | (7,539) | (4,525) |

| Derivative financial instruments | 26 | (135) | (271) |

| Contract liabilities | 21 | (649) | (1,392) |

| Lease liabilities | 27 | (643) | (550) |

| Provisions | 21 | (946) | (381) |

| Other liabilities | 28 | (1,812) | - |

| Total Current Liabilities | (11,724) | (7,119) | |

| Net Current Assets | 32,958 | 40,610 | |

| Non-Current Liabilities | |||

| Lease liabilities | 27 | (1,352) | (1,145) |

| Provisions | 21 | (1,493) | (1,627) |

| Other liabilities | (43) | - | |

| Total Non-Current Liabilities | (2,888) | (2,772) | |

| Total Liabilities | (14,612) | (9,891) | |

| Net Assets | 66,434 | 65,669 | |

| Equity | |||

| Called up share capital | 29 | 5,688 | 53,473 |

| Share premium | 29 | 22,872 | 215,121 |

| Share-based payment reserve | 29 | 8,129 | 7,328 |

| Merger reserve | 29 | 264,188 | - |

| Accumulated losses | 29 | (232,164) | (208,070) |

| Currency translation reserve | 29 | (2,318) | (2,222) |

| Other reserves | 29 | 39 | 39 |

| Total Equity | 66,434 | 65,669 |

1Refer to note 1

The above consolidated statement of financial position should be read in conjunction with the accompanying notes.

The financial statements were authorised by the Board of Directors and authorised for issue on 29 May 2026 and were signed on its behalf by:

Adam Howard

Director

Consolidated Statement of Changes in Equity

As at 31 December 2025

| Called up Share Capital | Share Premium | Share-based Payment Reserve | Accumulated Losses | Currency Transla-tion Reserve | Merger Reserve | Other Reserves | Total | |

| £000 | £000 | £000 | £000 | £000 | £000 | £000 | £000 | |

| At 1 January 2025 | 53,473 | 215,121 | 7,328 | (208,070) | (2,222) | - | 39 | 65,669 |

| Loss for the year | - | - | - | (24,094) | - | - | - | (24,094) |

| Other Comprehensive Income | ||||||||

| Foreign currency translation differences | - | - | - | - | (96) | - | - | (96) |

| Total Comprehensive Loss for the Year | - | - | - | (24,094) | (96) | - | - | (24,190) |

| Transactions with Owners in their Capacity as Owners | ||||||||

| Group reorganisation adjustment | (53,473) | (215,121) | - | - | - | 268,594 | - | - |

| Shares issued on redomiciliation | 61,679 | (61,679) | - | |||||

| Reduction of share capital | (57,273) | - | 57,273 | - | ||||

| Investment funding arrangement, net of transaction costs | 1,282 | 22,872 | - | - | - | - | - | 24,154 |

| Share-based payments | - | - | 801 | - | - | - | - | 801 |

| Total Contributions by Owners | (47,785) | (192,249) | 801 | - | - | 264,188 | - | 24,955 |

| At 31 December 2025 | 5,688 | 22,872 | 8,129 | (232,164) | (2,318) | 264,188 | 39 | 66,434 |

The above consolidated statement of changes in equity should be read in conjunction with the accompanying notes.

As at 31 December 2024 (Unaudited)1

| Called up Share Capital | Share Premium | Share-based Payment Reserve | Accumul-ated Losses | Currency Transla-tion Reserve | Other Reserves | Total | |

| £000 | £000 | £000 | £000 | £000 | £000 | £000 | |

| At 1 January 2024 | 51,348 | 162,883 | 6,683 | (185,273) | (1,867) | 39 | 33,813 |

| Loss for the year | - | - | - | (22,797) | - | - | (22,797) |

| Other Comprehensive Income | |||||||

| Foreign currency translation differences | - | - | - | - | (355) | - | (355) |

| Total Comprehensive Loss for the Year | - | - | - | (22,797) | (355) | - | (23,152) |

| Transactions with Owners in their Capacity as Owners | |||||||

| Investment funding arrangement, net of transaction costs | 2,125 | 52,234 | - | - | - | - | 54,359 |

| Exercise of share options | 4 | - | - | - | - | 4 | |

| Share-based payments | - | - | 645 | - | - | - | 645 |

| Total Contributions by Owners | 2,125 | 52,238 | 645 | - | - | - | 55,008 |

| At 31 December 2024 | 53,473 | 215,121 | 7,328 | (208,070) | (2,222) | 39 | 65,669 |

1Refer to note 1

The above consolidated statement of changes in equity should be read in conjunction with the accompanying notes.

Consolidated Statement of Cash Flows

For the year ended 31 December 2025

| 2025 | 2024 (Unaudited)1 | ||

| Note | £000 | £000 | |

| Cash Flows from Operating Activities | |||

| Cash used in operations | 14 | (17,682) | (26,147) |

| Interest received | 475 | 1,222 | |

| Interest paid | (1) | (13) | |

| Net Cash Outflow from Operating Activities | (17,208) | (24,938) | |

| Cash Flows from Investing Activities | |||

| Acquisition of property, plant and equipment | 16 | (1,507) | (1,294) |

| Acquisition of property, plant and equipment for battery project under construction | 16 | (13,938) | - |

| Prepayments of property, plant and equipment for battery project under construction | (1,558) | ||

| Grant income received against capital projects | 31 | 7,499 | - |

| Deposit on right-of use assets | - | (7) | |

| Net Cash Outflows from Investing Activities | (9,504) | (1,301) | |

| Cash Flows from Financing Activities | |||

| Payment of lease liabilities | 27 | (870) | (768) |

| Sublease deposit received | 43 | - | |

| Sublease payments received | 19 | 94 | 44 |

| Proceeds from the issue of share capital | 25,000 | 57,383 | |

| Proceeds from the exercise of share options and warrants | - | 4 | |

| Payment of transaction costs for the issue of share capital | (846) | (3,001) | |

| Net Cash Inflow from Financing Activities | 23,421 | 53,662 | |

| Net increase/(decrease) in cash and cash equivalents | (3,291) | 27,423 | |

| Cash and cash equivalents at the beginning of the year | 32,352 | 5,014 | |

| Effects of exchange rate changes on cash and cash equivalents | (272) | (85) | |

| Cash and Cash Equivalents at the End of the Year | 28,789 | 32,352 |

1Refer to note 1

The above consolidated statement of cash flows should be read in conjunction with the accompanying notes.

Notes

1 General Information

Invinity Energy Systems plc (the 'Company') is a public company limited by shares incorporated and domiciled in the UK. The registered office address is Room 3.03, 24 Chiswell Street, London, EC1Y 4TY.

The Company is quoted on the AIM Market of the London Stock Exchange with the ticker symbol IES.L.

During the year, the Group undertook a corporate reorganisation to redomicile the parent company from Jersey to the UK. As part of this reorganisation, a new UK-incorporated parent entity, Invinity Energy Systems plc, was inserted at the top of the Group through a share-for-share exchange. The transaction resulted in the Company becoming the ultimate parent of the Group. The reorganisation did not result in a change in the underlying business, operations, or economic substance of the Group and has been accounted for as a group reconstruction.

The comparative information presented has been derived from the consolidated financial statements previously audited for the predecessor group. While those financial statements related to a different legal entity, the underlying business and operations are unchanged. Accordingly, the Directors consider the comparative information to be representative of the Group's financial performance. The auditor's report on the current period financial statements does not extend to the comparative information in respect of the prior period. Therefore, the comparative information, including the notes, is presented as unaudited.

The prior year comparatives are unchanged from the previously published audited consolidated financial statements of the Group.

The principal activities of the Company and its subsidiaries (together the 'Group') relate to the manufacture and sale of vanadium flow battery systems and associated installation, warranty and other services.

2 Accounting Policies

Basis of Preparation

These consolidated financial statements have been prepared in accordance with International UK-adopted International Accounting Standards, the associated interpretations issued by the IFRS Interpretations Committee (together 'IFRS').

The accounting policies applied in preparing these consolidated financial statements are set out below. These policies have been consistently applied throughout the period and to each subsidiary within the Group.

The financial statements have been prepared under the historical cost convention except where stated.

Basis of Consolidation

Subsidiaries are all entities over which the Company has control. The Company controls an entity when it is exposed to, or has rights over, variable returns from its involvement with the entity and can affect those returns through its ability to exercise control over the entity. Subsidiaries are consolidated in the Group financial statements from the date at which control is transferred to the Company.

Subsidiaries are deconsolidated from the date that control ceases. The ability to control an entity may cease because of the sale of a subsidiary or other change in the Company's shareholding in that subsidiary, voting rights or board representation.

Transactions and balances between companies forming part of the Group together with any unrealised income and expenses arising from intra-group transactions are eliminated in the preparation of the consolidated financial statements of the Group.

Refer to note 35 - Group entities

Going Concern

The Directors have made an assessment of going concern covering the period from the date of approval of the financial statements to June 2027 and in making this statement, have prepared a cash flow forecast covering this period. The Directors have also considered whether there are any significant events expected to arise beyond the going concern period.

The forecast indicates that the Group expects to remain cash positive during the going concern period, without the requirement for further fundraising. This forecast includes judgements and estimates regarding income from pipeline projects, expected costs of delivering the contracts, and cost mitigation measures including the deferral of discretionary expenditure.

In order to fund expansion of the business, the Directors anticipate that additional funding would be required. The Directors have considered the availability of potential funding sources and the Group's track record in accessing capital markets in forming this assessment.

Invinity has prepared a downside cash forecast for the purposes of the going concern evaluation, which excludes all pipeline contracts that are not yet signed. In this scenario, the forecast assumes a reduction or deferral of costs in order to preserve cash without additional funding. If required, the Directors consider that the Group has the ability to reduce or defer costs without adversely affecting the short-term delivery of contracted income in downside forecast. The outcome of this scenario is that the Company has sufficient cash through the going concern period.

On the basis of this assessment, the Directors are satisfied that the Group has sufficient resources to continue in operation for the going concern period. Accordingly, the financial statements have been prepared on a going concern basis.

New Standards, Amendments and Interpretations Effective and Adopted by the Group in 2025

Amendments to existing standards previously issued by the IASB with effective dates during the year ended 31 December 2025 are summarised below. There was no effect on the Group's consolidated financial statements for the year ended 31 December 2025 as a result of the adoption of these amendments.

Amendments to 'IAS 21 The Effects of Changes in Foreign Exchange Rates - Lack of Exchangeability'

The Group has adopted the amendments to IAS 21 for the first time in the current year. The amendment clarifies the assessment of exchangeability and the determination of an exchange rate when exchangeability is lacking. The adoption of the amendment did not have a material impact on the Group's financial statements.

New Standards and Interpretations Not Yet Adopted

Certain new accounting standards and interpretations have been published that are not mandatory for 31 December 2025 reporting periods and have not been early adopted by the Company.

| Applicable Standard | Key requirements or changes in accounting policy |

| IFRS 9 Financial Instruments and IFRS 7 Financial Instruments: Disclosures - Classification and measurement of financial instruments Effective for periods beginning on or after 1 January 2026 |

In May 2024, the International Accounting Standards Board (IASB) amended IFRS 7 and IFRS 9, which includes clarifications on recognition and derecognition dates of certain financial assets and liabilities, including exceptions for liabilities settled through electronic cash transfer systems. |

| Annual Improvements to IFRS Accounting Standards - Volume 11 Effective for periods beginning on or after 1 January 2026 |

- IFRS 1 First-time Adoption of International Financial Reporting Standards - Hedge accounting by a first-time adopter; - IFRS 7 Financial Instruments: Disclosures - Gain or loss on derecognition - IFRS 7 Financial Instruments: Disclosures - Deferred difference between fair value and transaction price; - IFRS 7 Financial Instruments: Disclosures - Credit risk disclosures - IFRS 9 Financial Instruments - Lessee derecognition of lease liabilities; - IFRS 9 Financial Instruments - Transaction price; - IFRS 10 Consolidated Financial Statements - Determination of a De Facto Agent; and - IAS 7 Statement of Cash flows - Cost method. |

| IFRS 18 Presentation and Disclosure in Financial Statements Effective for periods beginning on or after 1 January 2027 |

IFRS 18 will replace IAS 1 Presentation of Financial Statements. The amendment impacts presentation and disclosure of the consolidated income statement with new defined categories being operating, investing and financing to provide a consistent structure. Disclosures about Management-defined Performance Measures (i.e. certain non-GAAP measures) will have to be disclosed in the financial statement with reconciliations to GAAP measures. The new standard will also provide guidance on grouping of information (aggregation/disaggregation). The standard will be applied from its mandatory effective date of 1 January 2027. Final impact assessment and transition activities will take place during 2026 and with the main impacts expected on the presentation of the consolidated statement of profit and loss. |

| IFRS 19 Subsidiaries without Public Accountability: Disclosures Effective for periods beginning on or after 1 January 2027 |

In May 2024, the Board issued IFRS 19 Subsidiaries without Public Accountability: Disclosures, which allows eligible entities to elect to apply reduced disclosure requirements while still applying the recognition, measurement and presentation requirements in other IFRS accounting standards. Unless otherwise specified, eligible entities that elect to apply IFRS 19 will not need to apply the disclosure requirements in other IFRS accounting standards. |

The Directors are evaluating the impact that these standards will have on the financial information of the Group.

Foreign Currency

Presentation Currency

The consolidated financial statements are presented in Great British Pounds (GBP) rounded to the nearest thousand (£000), except where otherwise indicated.

Functional Currency

Items included in the financial information of the individual companies that comprise the Group are measured using the currency of the primary economic environment in which each subsidiary operates (its functional currency).

Foreign Currency Transactions

Transactions in currencies other than an entity's functional currency (foreign currencies) are translated using the exchange rate on the date of the transaction. Foreign exchange gains and losses resulting from the settlement of transactions denominated in a foreign currency are translated into functional currency using the relevant exchange rate at the date of the transaction.

Foreign exchange gains and losses resulting from the settlement of foreign currency transactions and from the translation at the balance sheet date of monetary assets and liabilities denominated in foreign currencies, are recognised in the consolidated statement of comprehensive loss within gains/(losses) on foreign currency transactions.

Foreign currency gains/(losses) realised on the retranslation of subsidiaries as part of the year-end consolidation are recorded in the translation reserve that forms a part of shareholders' funds in the consolidated financial statements of the Group.

Foreign Currency Operations

Subsidiaries of the Company may have functional currencies that are different from that of the Company. Since the Group financial statements are presented in GBP, the assets and liabilities of foreign currency subsidiaries consolidated into these financial statements are translated into the Group's presentational currency using exchange rates prevailing at the end of the reporting period. Income and expense items are similarly translated using the average rate for each month during the year. The exchange rates on the actual dates of transactions are used where exchange rates fluctuate significantly within a month. Exchange differences arising on consolidation are recognised in other comprehensive income and are accumulated as part of shareholder's equity.

Operating Segments

The Group is organised internally to report to the Executive Directors as a whole. The Executive Directors comprise the Chief Executive Officer, the President and the Chief Financial Officer. The Executive Directors, as a group, have been determined, collectively, to prosecute the role of chief operating decision maker of the Group. The chief operating decision maker is ultimately responsible for entity-wide resource allocation decisions, the evaluation of the financial, operating and ESG performance of the Group.

The Group's activities have been determined to represent a single operating segment being the provision of vanadium flow batteries and ancillary services, principally comprising installation and integration services, and the provision of extended warranties for battery units sold.

Revenue

The Group generates revenue from the sale of battery storage systems integration hardware, installation, extended warranty and other services. These multiple elements are separate performance obligations that are derived from contractual arrangements with customers. The sales contracts do not include a general right of return.

For contracts that contain multiple elements or promises, the Group accounts for individual goods and services separately if they are distinct. A product or service is distinct if it is separately identifiable from other items in the agreement and where a customer can benefit from the good or service on its own or together with other resources that are readily available.

The consideration paid for each performance obligation is typically fixed. A significant portion of the aggregate payment due under a contract for sale is normally due before delivery or completion of the service. The total consideration under the contract is allocated between the distinct performance obligations contained in the contract based on their stand-alone selling prices. The stand-alone selling price is estimated using an adjusted market assessment approach that looks to industry benchmarks for certain standalone products or services. For other performance obligations, stand-alone selling price is estimated based on established processes, including budgeting tools, market labour rates and third-party quotes.

The Group measures revenue based on the consideration specified in the contracts for sale with customers. Revenue is recognised when a performance obligation is satisfied by transferring control over a good or service to a customer. With respect to the battery system, associated control systems and integration hardware, control is transferred at a point in time and is usually based on the contractual shipping terms. In certain instances, the battery system and integration hardware may be ready for delivery although the customer is not ready to receive the product. The Group will recognise revenue in accordance with IFRS 15 as a bill-and-hold arrangement if all of the following conditions are satisfied:

§ the reason for the bill-and-hold arrangement is substantive;

§ the battery systems and hardware are identified separately as belonging to the customer;

§ the battery systems and hardware are currently ready for physical transfer to the customer; and

§ the Company does not have the ability to use the product or to direct it to another customer.

With respect to the services that includes installation and commissioning, the performance obligation is usually satisfied at a point in time when a commissioning certificate or site performance report has been issued to the customer. Revenue excludes any taxes such as sales taxes, value added tax or other levies that are invoiced and collected on behalf of third parties, such as government tax authorities.

In addition, under the terms of its contracts for sale, the Group may be responsible for other services such as storing and delivering battery systems to its customers. When this is the case, the Group will invoice the relevant customer for, and will recognise as revenue, any charges incurred together with any associated handling costs. Revenue is recognised for the storage services over time as the services are delivered and for shipping services at a point in time when the goods are delivered to the agreed upon location. The related costs incurred by the Group for storage, shipping and handling services are recognised as cost of sales concurrent with the recognition of the associated revenue.

The Group may also enter into arrangements to license its intellectual property and associated technical know-how. Royalty revenue from licences that provide a right to use intellectual property is recognised at the point in time when the customer obtains control of the licence. This occurs when the customer obtains the ability to direct the use of and derive substantially all of the remaining benefits from the licensed intellectual property without further substantive ongoing obligations from the Group.

Grant Income

Government and other grants received are recognised in the consolidated statement of profit and loss in the period that the related expenditure is incurred.

Grants relating to income are recognised in profit or loss on a systematic basis over the periods in which the Group recognises the related costs. Such grants are presented as a reduction of the related expense line or as other items of operating income.

Grants relating to the acquisition or construction of assets are recognised by deducting the grant from the carrying amount of the asset, resulting in a reduced depreciation charge over the asset's useful life.

Grant income received in advance of the associated expenditure is presented as deferred income within other liabilities. Amounts are recognised in profit and loss as the associated expenditure is incurred or, where applicable, deducted from the carrying amount of the related capital expenditures.

Grant income receivable is presented within other assets until such time as it can be claimed or is received.

Finance Income and Costs

Finance income comprises interest on cash deposits, foreign currency gains and the unwind of discount on any assets that are carried at amortised cost. Interest income is recognised as it accrues using the effective interest rate method.

Finance costs include foreign currency losses and the unwind of the discount on any liabilities held at amortised cost, such as lease liabilities arising from lease contracts.

Employee Benefits

Short-term Benefits

Benefits provided to employees that are short-term in nature are recognised as expenses in the statement of profit and loss as the related service is provided. The principal short-term benefits given to employees are salaries, associated holiday pay and other periodic benefits such as healthcare and pension contributions made by the Group for the benefit of the employee. A liability is recognised for the amount expected to be paid under short-term cash bonus plans if there is either a present legal or constructive obligation to pay the amount and the amount can be reliably estimated.

Share-based Payments

The Group operates equity-settled share-based compensation plans, under which it compensates employees for services rendered through the issue of equity instruments, deferred share awards or options to subscribe for ordinary shares of the Group. The fair value of the employee services received in exchange for the grant of the equity instruments, shares or options is recognised as an expense. The total amount to be expensed is determined by reference to the fair value of the options granted:

§ including any market conditions (for example, the Group's share price);

§ excluding the impact of any service and non-market performance vesting conditions (for example, profitability, sales, growth targets, and the requirement to remain as an employee of the Group over a specified period); and

§ including the impact of any non-vesting conditions.

Non-market performance and service conditions are included in the assumptions regarding the number of options that are expected to vest. The total expense is recognised over the vesting period, which is the period over which all the specified vesting conditions are to be satisfied.

In some circumstances, employees may provide services in advance of the grant date and therefore the grant date fair value is estimated for the purposes of recognising the expense during the period between service commencement and the grant date.

At the end of each reporting period, the Group revises its estimates of the number of options that are expected to vest based on the non-market vesting conditions. It recognises the impact of the revision to original estimates, if any, in the consolidated statement of profit and loss, with a corresponding adjustment to equity.

Any social security contributions payable in connection with the grant of the share options is considered an integral part of the grant itself, and the charge will be treated as a cash-settled transaction.

Taxes

The total tax charge or credit recognised in the statement of profit and loss comprises both current and deferred taxes. Taxation is recognised in the consolidated statement of profit and loss except to the extent that it relates to a business combination or items recognised directly in equity or other comprehensive income.

Current Tax

The current tax charge is based on the taxable profit for the year. Taxable profit or loss is different from the profit or loss reported in the statement of profit and loss as it excludes items of income and/or expense that are taxable or deductible in other years (temporary differences) and it further excludes items that are never taxable nor deductible (permanent differences).

Deferred Tax

Deferred tax is the tax that is expected to be payable or recoverable on differences between the carrying value of assets and liabilities in the financial statements and the corresponding value of those assets and liabilities used to calculate taxable profit or loss.

Deferred tax assets are recognised for all deductible temporary differences, the carry forward of unused tax credits and any unused tax losses. Deferred tax assets are recognised to the extent that it is probable that taxable profit will be available against which the deductible temporary differences, and the carry forward of unused tax credits and unused tax losses can be utilised.

Deferred tax assets and liabilities are recognised using the liability method for all taxable temporary differences, except in respect of taxable temporary differences associated with investments in subsidiaries and associates. Where the timing of the reversal of temporary difference arising from such investment related assets and liabilities can be controlled and it is probable that the temporary difference will not reverse in the foreseeable future then the Group does not recognise deferred tax liabilities on these items.

A deferred tax asset or liability is not recognised if a temporary difference arises on initial recognition of an asset or liability and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss.

Current and deferred tax is calculated using tax rates and laws that have been enacted or substantively enacted at the balance sheet date. Deferred tax balances are presented on a gross basis. Refer to note 18, deferred tax balances.

Earnings per Share

The Group presents basic and diluted earnings per share ("EPS") data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss attributable to ordinary shareholders of the Company by the weighted average number of ordinary shares outstanding during the year.

Diluted EPS is determined by adjusting the weighted average number of ordinary shares outstanding used in the EPS calculation to include all potentially dilutive ordinary shares, which, in the case of the Company, represents additional shares that could be issued in relation to 'in-the-money' convertible notes, warrants or share options.

The effects of anti-dilutive potential ordinary shares are ignored in calculating diluted EPS. Anti-dilution is when an increase in earnings per share or a reduction in loss per share would result from the exercise of such options, warrants or convertible instruments.

Intangible Assets

Goodwill

The Group allocates the fair value of the purchase consideration on the acquisition of a subsidiary to the assets acquired and liabilities assumed based on an assessment of fair value at the acquisition date. Any excess of purchase consideration is recognised as goodwill. Where goodwill is recognised, it is allocated to the cash generating units (CGUs) in a systematic manner reflective of how the Group expects to recover the value of the goodwill. Because the Group has been determined to consist of a single business unit, the carrying value of goodwill is tested for impairment based on the recoverable value of the Group as a whole.

Goodwill is not amortised but is tested for impairment on an annual basis, and the Group will also test for impairment at other times if there is an indication that an impairment may exist. Determining whether goodwill is impaired requires an estimation of recoverable amount based on the higher of its value in use and fair value less costs of disposal. The key estimates are therefore the selection of the suitable discount rates and the estimation of future growth rates which may depend on specific risks and the anticipated economic and market conditions related to the CGU.