Prior Year Accruals: Understanding Financial Adjustments

Accurate financial reporting is key to a company's trustworthiness. Prior year accruals are essential in this regard. They make sure financial statements reflect revenues and expenses correctly, based on when they happen, not when cash is exchanged. This method follows Generally Accepted Accounting Principles (GAAP). It gives a true picture of a company's financial health.

Journal entries for accrued expenses and revenues are crucial. They help keep financial records consistent. Understanding these financial adjustments is critical for accurate accounting.

Key Takeaways

- Prior year accruals ensure financial results are recorded in the right period, following GAAP.

- They maintain integrity in financial statements by recording earnings not yet received and expenses not yet paid.

- Accruals help correct the income statement and make the balance sheet more accurate.

- They are automatically reversed at the start of the new financial year to avoid expense duplication.

- The detailed process of accrual accounting is necessary for a clear financial understanding of a company.

- Using systems like Prime Financials makes it easier to record important transactions accurately and efficiently.

- Managing prior year accruals through the Controller's office integrates these adjustments smoothly into annual reports.

What Are Prior Year Accruals?

Prior year accruals are crucial for accurate and compliant financial records. They relate to last year's transactions recorded in the next period's financial statements. This method matches revenues and expenses with the actual time they happen, not when money changes hands.

Definition and Importance

Accruals definition implies making adjustments for revenues earned or expenses incurred after the fiscal year ends. These adjustments are necessary under accrual accounting principles, key to GAAP (Generally Accepted Accounting Principles). Accrual accounting gives a clearer view of a company's financial health by recognizing economic events as they occur.

Key Principles of Accrual Accounting

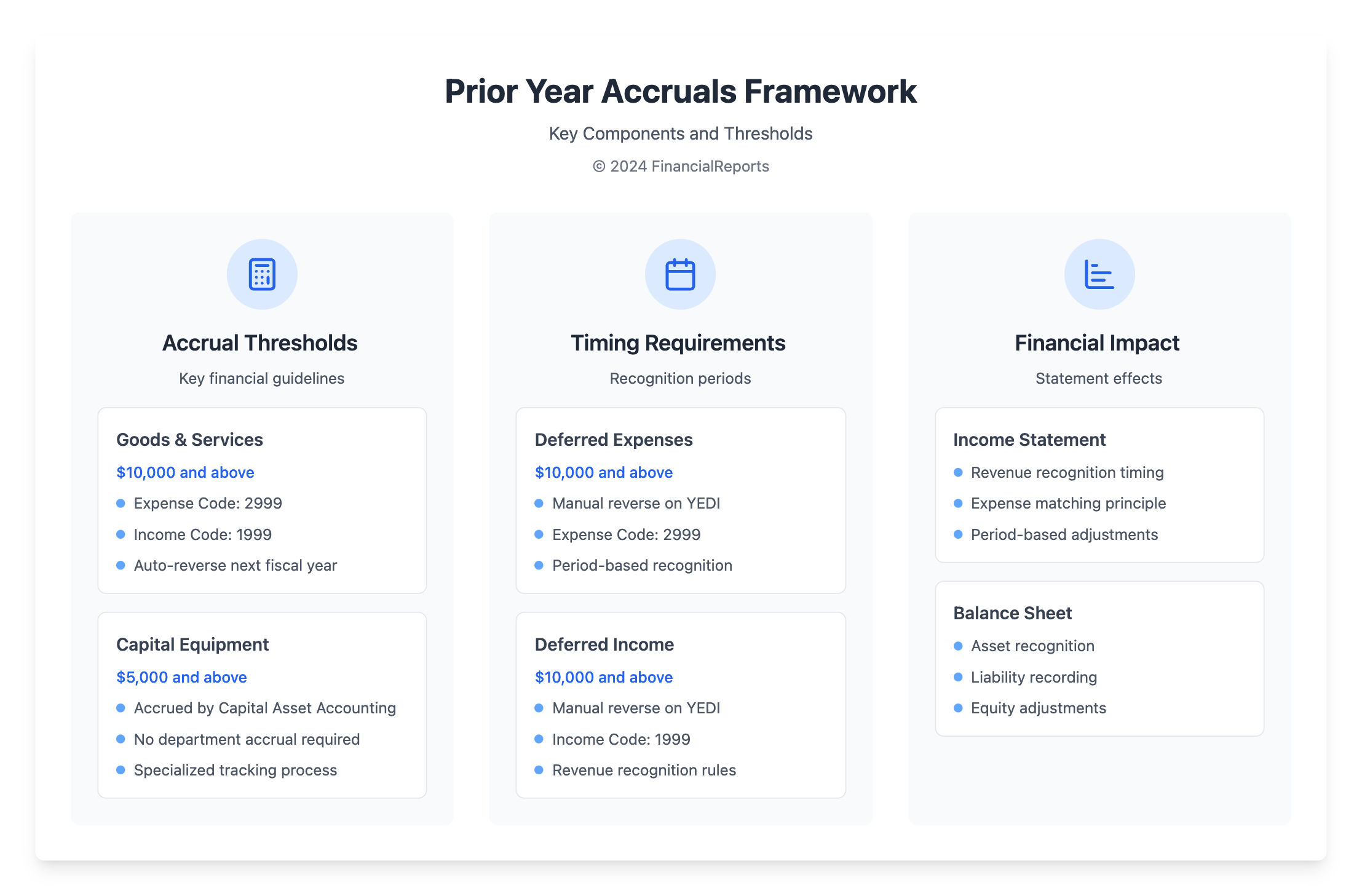

Accrual accounting's main purpose is to offer an accurate financial overview of a company. Below is a table showing guidelines for different items under these standards:

| Item Type | Threshold | Accrual Required | Code for Year-End Accrual | Reversal Procedure |

|---|---|---|---|---|

| Goods/Services Received | $10,000 and above | Yes | Expense: 2999 Income: 1999 |

Auto-reverse next fiscal year |

| Capitalized Equipment | $5,000 and above | Accrued by Capital Asset Accounting | Not required by departments | N/A |

| Deferred Expenses | $10,000 and above | Yes | Expense: 2999 | Manual reverse on YEDI |

| Deferred Income | $10,000 and above | Yes | Income: 1999 | Manual reverse on YEDI |

This guidance helps ensure accurate financial reporting for the year. Following these principles helps businesses stay credible and reliable. This makes it easier for stakeholders to make informed decisions.

The Role of Accruals in Financial Statements

Accrual accounting is key for showing a business's real financial state. It paints a clear picture of financial health. This section looks at how accruals play a big part in financial reports. We see their role in income statements, balance sheets, and cash flow.

We explore this through the eyes of expert financial practices. We examine how accruals work and what they mean.

Impact on Income Statements

Accruals change how income statements look. They let businesses recognize revenue when earned, not just when cash changes hands. This matches income and costs in the right period. It gives a true view of a company's earnings.

For example, accrued costs like salaries help compare costs with the income they help create. This sharpens profit checks and future money planning.

Effect on Balance Sheets

Accruals are crucial for accurate balance sheets. They show debts and resources yet to be dealt with in cash. This can be money owed for goods or sales not yet paid for. It shows real financial standing.

The University of San Francisco, for instance, records accrued costs and prepaid assets above $1000. This keeps their financial statements precise and responsible.

Significance for Cash Flow Management

Accrual accounting is vital for managing cash flow. It separates money earned from money received. This lets finance managers plan for cash needs better.

For groups like the Federal Columbia River Power System, following GAAP makes money flow easier to manage. These methods help keep cash flow steady. They ensure a business can keep running all year.

To sum up, using accruals in reports is essential. It gives a real and full view of a company's money situation. Accruals lead to clearer reporting. This builds trust with investors and meets rules.

Common Strategies for Recording Prior Year Accruals

Ensuring accurate financial reporting and transparency in year-end adjustments is crucial. Effective strategies for recording prior year accruals are necessary. These methods help keep financial statements true and reliable, giving a real picture of a company's financial health. We will now share some guidelines and best practices critical to this process.

Guidelines for Accurate Reporting

Understanding accrued revenues and expenses is key to record prior year accruals. These may include wages, utility bills, and other costs not yet paid. Also, they involve revenues earned but not yet received. It's important to document each financial activity in the correct fiscal period. Here are important points to consider:

- Accrual Documentation: Keep detailed records of all accrued expenses and revenues, noting the nature and time of every transaction.

- Regular Reviews: Do monthly and quarterly checks to ensure all financial activities are recorded. This reduces year-end omission risks.

- Use of Adjusting Journal Entries: Apply journal entries for accruals, deferrals, and estimates. This helps align financial reports with actual economic events.

Best Practices for Year-End Adjustments

Year-end adjustments are key for compliant and clear financial reporting. These adjustments ensure the activities of the financial period are correctly represented. This assists in decision-making and planning. Following these practices is critical:

- Comprehensive Closing Procedures: Set up strict closing procedures to catch any missed activities affecting financial results.

- Verification of Accruals: Check all recorded accruals against invoices and payment statements for accuracy and completeness.

- Fostering Communication: Promote open discussion between accounting and other departments to capture all financial information accurately.

| Type of Journal Entry | Description | Examples |

|---|---|---|

| Accruals | Entries made to record revenues and expenses that are earned or incurred but not yet received or paid. | Revenue from services delivered but not yet billed, Expenses like unpaid rent or wages. |

| Deferrals | Entries to account for revenue received in advance or expenses paid in advance. | Prepaid rent, Annual software subscriptions paid upfront. |

| Estimates | Entries that involve estimation, often used for items like depreciation or allowance for doubtful accounts. | Depreciation on office equipment, Bad debt expenses. |

By using these strategies and following best practices, organizations can ensure proper recording of prior year accruals. This enhances the accuracy and reliability of financial reporting. It supports not just regulatory compliance but also strategic financial management. In turn, this leads to more informed business decisions.

Challenges Associated with Prior Year Accruals

It's crucial to accurately manage prior year accruals to ensure financial reports are correct. Accrual accounting faces various challenges. These include finding missing accruals and handling time differences.

Identifying Missing Accruals

Finding missing accruals is a big challenge. This issue can change how an organization's finances look. Sometimes, transactions are not fully recorded at the end of the fiscal year. This leads to big differences in reported incomes and expenses. These discrepancies affect decisions and future financial planning.

- Impact on Financial Statements: Unrecorded missing accruals can change financial numbers. This can lead to misunderstandings of a company's financial status.

- Compliance Risks: Wrong financial reports from missing accruals might break accounting rules. This could lead to legal issues.

- Rectification and Audit Concerns: Fixing missing accruals takes a lot of work. It can also make audits harder.

Managing Timing Differences

Handling timing differences is another key issue. These differences occur when transactions are recorded in different periods than they happened. This can cause earnings to fluctuate. Such fluctuations make analyzing finances harder.

- Matching Principle: It's hard to follow the matching principle with big timing differences. This principle tries to match costs with related incomes.

- Budget Forecasting: Timing differences can mess up budgets. Forecasts may not match actual money movements.

- Stakeholder Perceptions: If accruals and real cash flows don't match, it can confuse investors. This might affect stock prices or loan terms.

To tackle these issues, detailed record-keeping is essential. A strong system of internal controls is also vital. Using sophisticated accounting software can help manage complex accrual situations. Paying attention to the details of each transaction and aiming for accuracy can reduce risks. This will make financial reporting more reliable.

Legal and Regulatory Considerations

The financial reporting landscape is strictly shaped by laws and rules. This includes GAAP in the United States and International Financial Reporting Standards (IFRS) globally. These guidelines are key to keeping things uniform and clear, affecting how businesses manage accrual accounting rules. Companies must understand and follow these to show their true financial status and stay in line with regulations.

Compliance with GAAP

For US companies, following GAAP is a must. It sets out how to record transactions on an accrual basis. This involves rules on how to recognize revenue and match expenses. These are important for showing the company's financial well-being accurately. Sticking to these rules is legally needed and shows the company is trustworthy in its financial reports.

Implications of IFRS on Accrual Accounting

IFRS affects businesses worldwide, changing how they record and share financial information. Adopting IFRS helps standardize accounting practices internationally but comes with challenges. Especially for areas moving from local to global standards. It significantly changes financial reporting, requiring careful application in accruals, where transactions are recorded when they happen, not when cash changes hands.

It is essential to ensure IFRS implications are well understood and applied correctly. This helps make financial statements comparable and consistent worldwide. It also helps companies attract foreign investment and expand into new areas.

How Prior Year Accruals Affect Tax Reporting

Understanding prior year accruals is key for right tax reporting. The accrual method is a main accounting way. It decides when to count income and expenses for a business.

Tax Implications of Accruals

Accrual tax implications are big for a company's financial statements. With the accrual method, income is reported in the year it's earned. Expenses are counted in the year they happen. This might not match with when cash moves, affecting taxable income and tax dues a lot.

Businesses must keep their accounting consistent to follow IRS rules. This ensures a true view of a company's financial state is shown.

Timing of Revenue and Expense Recognition

The rule under accrual accounting says revenue is counted when it's made. This is regardless of when cash comes in. On the other side, expenses are recognized when they happen, not when paid. This can lead to differences between cash flow and reported earnings.

These differences impact tax dues and planning. Companies need to manage these variances well. They should aim for the best tax results and follow tax laws.

Following the accrual method shows a company's financial health better. Yet, the timing of income and expense recognition can make tax time tough. It might not show how much cash a business really has. Good tax plans and accounting systems are must-haves for true tax reports. They help align with business goals and follow tax rules.

Audit Considerations for Prior Year Accruals

Auditing prior year accruals needs careful work by auditors. It ensures financial statements are true and fair. New rules from the PCAOB start on December 15, 2025. Auditors must change and improve their methods for these accruals.

The Audit Process for Accruals

The audit process for prior year accruals follows specific steps. These steps confirm the rightness of the accruals on the financial statements. It includes checking transactions and looking at changes as the new PCAOB rules say. Accountants have to make sure these checks closely follow the set accounting rules.

This careful checking is crucial. The SEC requires companies to have an accountant review their financial reports before they file them.

Addressing Auditor Concerns

Auditors mainly check if there's enough reliable proof for the accruals. They look closely at the accounting estimates made by managers. Auditors make sure these are sensible and follow generally accepted accounting principles (GAAP).

They also review the manager's processes and rules that shape these estimates. The goal is to reduce mistakes and biases that could affect the financial reports a lot.

| Aspect | Guideline | Effectiveness Date |

|---|---|---|

| Amendments to Audit Considerations | PCAOB Standards | December 15, 2025 |

| Review of Interim Financial Information | SEC Independence Requirement | Continuous (Prior to Q report filings) |

| Accounting Estimates Evaluation | AS 4105 Guidance | Audits post January 1, 1989 |

| Internal Controls for Financial Reporting | Integrated Audit Approach | As per audit schedule |

Auditors should keep a professional skepticism during their audit. Staff Audit Practice Alerts No. 4, No. 5, and No. 15 offer guidance on this. They make sure management's significant estimates have solid proof and accurately show the company's finances.

Tools and Software for Managing Accruals

Financial tech has evolved. Now, it gives financial experts powerful tools for easier accrual management. Using advanced accounting software is key for precise and quick financial reports as financial tasks get more complex.

Popular Accounting Software Options

Many financial teams pick from different software to handle accruals well. QuickBooks Online Advanced has rich features that make it worth more than its Plus version. Meanwhile, Sage Intacct's cost is higher but it offers top-notch capabilities. Zoho Books provides scalable plans and a free trial for any business size.

Benefits of Automation in Accrual Management

Modern financial automation tools boost data accuracy by reducing human mistakes. Tools like Glean.ai stand out with automatic accrual features, improving efficiency and detail in reporting. They help with managing multiple entities, instant reporting, and intricate bank reconciliations for smoother financial operations.

| Software | Key Features | Support Options | Price Range |

|---|---|---|---|

| QuickBooks Online Advanced | Automated accrual calculations, multi-entity management | Live chat, email, 24/7 assistance | More than double the cost of Plus version |

| Sage Intacct | Real-time financial reporting, comprehensive documentation | Email support, comprehensive documentation | Higher than QuickBooks Online Advanced |

| Zoho Books | Flexible pricing plans, automated bank reconciliation | Live chat, email support, 24/7 assistance | Various plans including free trial |

| Glean.ai | One-click accrual settings, real-time accrual tracking | Email support, documentation | Custom pricing based on features |

By using accrual accounting, we record revenues and expenses as they happen. This method is much better with accounting software tools. Sophisticated platforms boost financial insights. They also free up finance pros to focus on strategic analysis and making smart decisions.

Case Studies: Successful Management of Prior Year Accruals

Studying real-world case studies helps us grasp the essence of successful accrual management. We delve into how different organizations handle this complex issue. It teaches us valuable financial lessons and steers companies towards improved compliance and efficiency.

Real-World Examples

Take Airbase, for instance. It's a platform that simplifies the accrual process for many firms. Airbase calculates accruals automatically, covering both approved purchases and requests still pending. This ensures financial reports are up-to-date and comply with GAAP standards. Its efficiency in handling variable and seasonal accruals is remarkable, adjusting easily to shifts in business activity and time.

Another key example is Georgia's State Accounting Office (SAO). They prepare an Annual Comprehensive Financial Report (ACFR) closely following GAAP guidelines. The SAO combines accrual and cash accounting for government funds. This makes sure revenues are recognized accurately, aiding state managers and policy makers in their decisions.

Lessons Learned from the Cases

- Timeliness and Accuracy: Essential in accrual accounting, shown by tools like Airbase. Accurate accrual recording keeps financial statements current and correct.

- Compliance and Adaptability: Firms need to adjust their accounting to stay within the law. The SAO's mixed accounting method shows the value of being flexible to adapt to laws and policy changes.

- Technology Integration: Using new tech reduces mistakes and boosts productivity. Moving to software from manual processes improves how accruals are handled.

These case studies reveal the best practices and common issues in successful accrual management. They cement the key financial lessons that any organization can use to enhance its financial reporting.

Future Trends in Accrual Accounting

Markets are changing fast, and accrual accounting is changing with them. It uses principles from the Generally Accepted Accounting Principles (GAAP). This type of accounting is key for showing how well a business is doing financially. The move to a more tech-based world means financial reporting innovations and focusing more on data.

The Impact of Technology

Technology is changing accrual accounting in big ways. It makes things faster and can predict financial trends better. Software now does a lot of the work, which cuts down on mistakes and the risk of wrong accrual estimates. AI helps us look at big amounts of data better, making accruals more precise. In the past, the link between accruals and cash flows was strong. Now, that link has almost disappeared. This shows how much accounting methods have improved. Technology and accrual accounting working together means financial experts can expect to see accurate, up-to-date information.

Emerging Best Practices in Financial Reporting

The link between accruals and cash flows is changing. More cash flow doesn't always mean fewer accruals now. This shows a new, more detailed way of handling financial records. It stresses the need for updated best practices that match today's complex market activities. Embracing future trends means being more open and making smarter choices. These trends affect all kinds of industries, not just ones with many physical assets. With 70% of companies dealing with accrued expenses, it's crucial to understand and use these new methods. This ensures financial reports are right and keeps people confident in the numbers.

FAQ

What are prior year accruals in accounting?

Prior year accruals are adjustments for money earned or spent in a past period but recorded in the next period's finances. This ensures financial reports are right, following accrual accounting rules.

Why are prior year accruals important?

They keep reports in line with GAAP and IFRS, ensuring earnings and costs match the right period. This gives a true view of a company’s health, important for investors and decision-makers.

How do accruals affect financial statements?

Accruals make sure income statements show real revenue and expenses. They also keep the balance sheet accurate by recording assets or liabilities correctly. This shows the company's true financial state.

What common strategies are used to record prior year accruals?

Companies check all year's transactions to find unrecorded revenue or expenses. Then, they make necessary adjustments. Keeping detailed records and checking regularly helps them stay accurate and follow rules.

How do companies address the challenges of missing accruals?

To avoid missed accruals, firms watch transactions closely, especially at year-end. They use strict checks and regular balance checks to find and fix mistakes quickly.

What are the implications of GAAP and IFRS on accrual accounting?

Following GAAP and IFRS means financial info is clear and comparable across entities and places. It requires detailed policies to properly handle how revenue and expenses are recorded.

How do prior year accruals impact tax reporting?

With accrual accounting, taxes may be due based on earnings and spends, not cash flow. This affects when taxes are paid, ensuring correct tax amounts are reported.

What are the audit considerations for prior year accruals?

Auditors check prior year accruals for their truthfulness and correctness. They confirm these entries match financial statements and follow the right accounting standards.

How can tools and software improve accrual management?

Modern software helps automate and correct accruals, cutting down errors. It gives live data and better accuracy, aiding in smart financial decisions.

Why are case studies on successful management of prior year accruals beneficial?

Case studies show how firms successfully handle prior year accruals. They offer lessons on best practices and clever solutions, helping others improve their accounting methods.

What are the emerging trends in accrual accounting?

Technology like AI and analytics is changing accrual accounting. It allows for more precise accrual tracking and timely, predictive financial reports.